China controls more than 85% of global polysilicon production, with production concentrated in regions that rely on coal-fired electricity. This extreme concentration creates an immediate supply bottleneck for European manufacturers, leaving clean energy deployment exposed to geopolitical strain and trade restrictions. The European Union has responded with ambitious legislation, setting a domestic clean technology manufacturing target of 40% by 2030.

RESiLICON, a Dutch startup founded in 2023, plans to challenge this status quo. By constructing an industrial-scale manufacturing plant in Delfzijl, the Netherlands, the company aims to produce high-purity polysilicon and essential specialty gases, all powered by renewable energy.

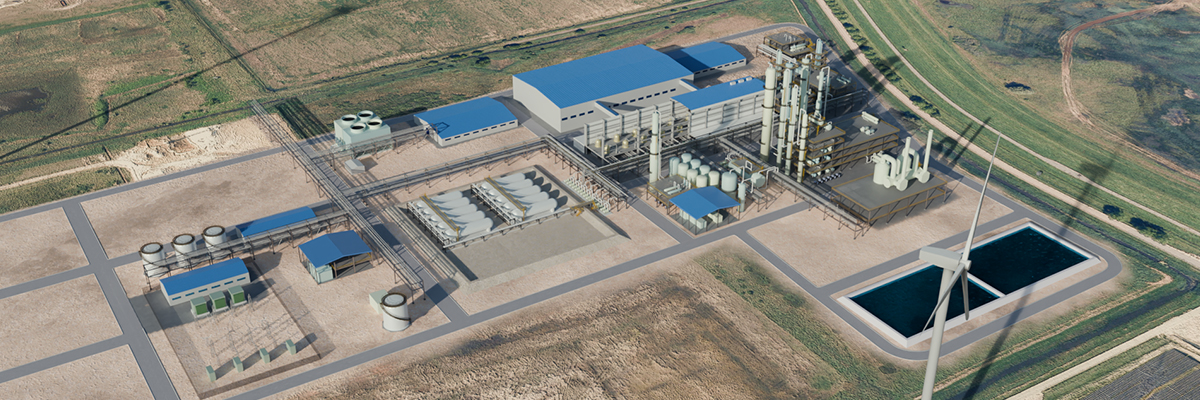

Image: RESiLICON

Key takeaways

- Strategic autonomy: RESiLICON aims to supply up to 26,000 MT of ultra-pure polysilicon annually, positioning the company to address critical European supply vulnerabilities by 2030.

- Diversified approach: The company targets three distinct markets, providing raw materials for semiconductors, solar energy components, and silicon-anode battery manufacturing.

- Technical integration: Partnering with Fluor and Advanced Material Solutions (AMS), the facility in Delfzijl utilizes specialized chemical processing to lower energy consumption by 30% with best-in-class technology.

- Regulatory friction: Although designated a strategic project under the Net-Zero Industry Act (NZIA), the company faces capital-scale-up challenges due to funding rules designed for established corporations.

Gosse Boxhoorn (left) and Remco Rijn (right)

Driving forces

Steering this ambitious initiative is a leadership team with deep roots in global industrial operations, solar manufacturing, and raw material refinement. Co-founder Gosse Boxhoorn is a veteran energy entrepreneur whose career spans management roles at Shell Solar and OTB Engineering. In 2003, he co-founded Solland Solar, a solar cell manufacturer that grew rapidly to 400 employees. His dedicated focus on securing a domestic raw material supply chain began in 2006, when he launched The Silicon Mine project, a pioneering effort to construct a solar-grade silicon plant in Limburg. This project ended due to the global financial crisis, and, in later years, the solar crises that hit all European solar companies at that time. CEO Remco Rijn brings more than 25 years of international corporate leadership. His extensive background features high-level management and executive project roles at major global institutions, including Shell, Philips, and the international credit insurer Atradius, providing the operational stamina and commercial scale necessary to manage the complex structural layout of a large-scale industrial facility.

Following an extensive interview conducted on 21 May 2026 with Boxhoorn and Rijn, we present a realistic assessment of the path to domestic industrial resilience.

The starting line

The vision for a domestic European silicon supply chain is not new, but the market conditions have shifted dramatically in recent years. What was the specific catalyst or 'turning point' that moved RESiLICON from a strategic concept to a high-priority industrial project?

Gosse Boxhoorn: The immediate spark came from a collective realization during the pandemic, when Europe found itself unable to manufacture basic medical masks domestically. It exposed deep structural vulnerabilities in our industrial baseline. My personal efforts in this sector go back to 2006, when we launched The Silicon Mine (TSM) project in Limburg. That project halted due to the global financial crisis and the subsequent collapse of European photovoltaic manufacturing. However, the foundational technical expertise never disappeared. The true turning point was the introduction of the EU Critical Raw Materials Act (CRMA), which officially placed silicon on the strategic priority list. With clear legislative recognition from Brussels, we established RESiLICON in the second quarter of 2023.

What is the ultimate dream and mission for the company, and what was the definitive catalyst that turned this from a strategic concept into a concrete plan for a facility in Delfzijl?

Gosse Boxhoorn: Our mission is to accelerate the energy transition while ensuring Europe retains a relevant position in the global clean technology ecosystem. Photovoltaics, fotonica, and the semiconductor industry share a common language, electrons and photons, and similar equipment. We cannot simply separate research from manufacturing, because when production moves away, development eventually follows. Selecting Delfzijl as our location was a highly strategic choice. First, the region offers direct infrastructure links to offshore wind power developments, ensuring access to renewable electricity at some of the lowest projected costs in Europe. Second, our refinement process utilizes chlorinated compounds. While our loop is fully closed and boasts minimal emissions through comprehensive recycling, operating a chlorine-based chemical process requires a highly specialized chemical cluster. Delfzijl - also with Nobian Industrial Chemicals already present - stands out as one of the few locations on the European map that satisfies all these logistical, ecological, and technical requirements.

Image: Unsplash

Market reality check

Chinese polysilicon prices often hit record lows due to massive economies of scale and low energy costs. Beyond the clear appeal of a local supply chain, what practical strategies will you use to keep your price point competitive and attractive for European module manufacturers?

Gosse Boxhoorn: Scale is absolute, which is why our blueprint scopes out a production volume of 13,000 MT per year in our initial phase, expanding to 26,000 MT per year. It is also critical to understand that the solar market is heavily distorted. Roughly half of global polysilicon production originates in Xinjiang, which many reports link to forced labor and to cheap, high-emission coal. Europe is implementing structural defensive measures, including the Carbon Border Adjustment Mechanism (CBAM), the Net-Zero Industry Act (NZIA), and strict forced-labor regulations, to establish a level playing field. Furthermore, we are not relying solely on solar. We are targeting three distinct high-value verticals: semiconductors, solar, and battery anodes. The semiconductor space, for example, demands extreme purity levels (up to 12N-grade) where Chinese producers do not dominate, allowing us to capture premium margins. However, tapping into the solar market is required to achieve economies of scale.

We have to understand that geographic independence is not cheap; production in Europe simply carries higher costs. However, if our strategic industry value chain is affected by geographic policy, the European automotive and defense industries will be affected similarly. So what is the price for security of supply we’re ultimately willing to pay?

High-level strategic support is essential, but building a facility with a €900 million capital requirement demands firm commercial backing. How is the process of securing long-term off-take agreements with European partners progressing?

Remco Rijn: The very first question any serious investor asks centers on off-take security. In the semiconductor sector, the demand for local supply and dual-sourcing options is immediate and highly proven. We recently announced a promising early-stage collaboration with a potential launching customer, TopSil, which validates this commercial track record. The solar market requires a bit more regulatory stability, as buyers need full certainty on how domestic content criteria will be enforced across all 27 EU member states. Meanwhile, the battery space represents an exciting, embryonic vertical. We are engaged in advanced discussions with silicon-anode battery pioneers like GDI and LeydenJar, structuring a balanced product mix of polysilicon, silane, and specialized industrial gases.

Infrastructure and technology

The Delfzijl facility is designed to be fully powered by renewable energy. Given the current grid congestion and intermittency challenges in the Netherlands, how do you plan to secure the 24/7 'firm' power required for a high-heat chemical process?

Remco Rijn: Securing a continuous, stable power profile is a substantial operational hurdle for any heavy chemical refinery. Our approach relies on the unique geographical advantage of the Groningen Sea Ports network, which handles the direct intake of major offshore wind assets. By positioning our facility right at the landing point of this clean generation, we mitigate a significant portion of national grid transit constraints.

You are working with technology from Advanced Material Solutions (AMS) to reduce energy consumption by a reported 30% compared to traditional manufacturing methods. What makes this specific process more efficient and sustainable?

Remco Rijn: Traditional manufacturing relies on multi-step cooling, solidifying, and mechanical breaking processes that consume immense amounts of electricity. The technical approach, developed alongside our partners AMS and the engineering firm Fluor, optimizes chemical vapor deposition directly in the gas phase. By maintaining the raw chemical components in a high-purity gaseous state for longer, we eliminate energy-intensive secondary processing steps. This clean loop design not only slashes our electrical overhead by nearly a third but also opens up opportunities to innovate downstream products directly from the gas phase, bypassing legacy manufacturing bottlenecks entirely.

Image: Unsplash

Policy and strategy

Being named a strategic project under the Net-Zero Industry Act (NZIA) is a major achievement for the company. What is the most significant practical change this status brings to your day-to-day development and permitting process?

Remco Rijn: The NZIA designation was a remarkable milestone that instantly put RESiLICON on the global industrial radar, providing valuable validation from international clean-technology experts. However, we must be entirely straightforward about the current reality: this framework does not automatically translate into immediate cash or direct financing. The European Commission is still assembling its funding mechanisms. A major structural bottleneck we experience daily is that European regulatory frameworks are built exclusively for established, corporate giants. Being asked to provide revenue statements spanning the last three years is a total killer phrase for a scaling company. We are actively lobbying Brussels and the Dutch Ministry of Economic Affairs to loosen these rigid state-aid rules, allowing nations to back vital industrial infrastructure with real execution speed. The electric car industry also did not hit its stride because of policy, government stimulus, or traditional players like Mercedes and Volkswagen. A new startup, Tesla, had to serve as the sector’s true wake-up call.

If Europe builds raw material capacity but continues to face a shortage of wafer and cell manufacturing, where will the domestic polysilicon go? Do you see the rest of the European supply chain expanding fast enough to match your timeline?

Remco Rijn: This supply chain imbalance is exactly why our business case does not rest solely on solar PV. Because we produce ultra-high-purity silicon and silane gases, our volume can seamlessly flow into the European semiconductor ecosystem, which is already mature, local, and actively seeking domestic dual-sourcing options. That being said, we are active members of the European Solar Manufacturing Council (ESMC) and Solar Power Europe, working to ensure the middle sections of the solar supply chain expand in parallel.

To bring this vision to life and give the project its next big push, what is the immediate next milestone for RESiLICON, and what specific types of commercial or strategic partners are you actively looking for right now?

Remco Rijn: Our current focus is on executing the comprehensive basic design and engineering phase alongside Fluor and AMS, with support from a €14 million seed round from regional development agencies, including NOM. Our ultimate horizon is securing the full €900 million required for our final investment decision (FID), slated for early 2027. Traditional venture capitalists are often a poor fit for heavy industrial scale-ups; they want to inject small capital and quickly extract a three-times return within a couple of years. We do not need short-term speculators. We are actively seeking long-term industrial partners, large infrastructure funds, and public-private alliances that possess the financial stamina and operational scale to build a lasting domestic ecosystem. Preferably, players from the European ecosystem, but we’re not excluding the option of foreign investment beyond the European border.

Future vision

Looking ahead to 2036, ten years from now, what is your ultimate vision for RESiLICON in terms of production volume, scale, and its role in the European clean energy ecosystem?

Remco Rijn: Our immediate operational target is to have our first commercial silicon rolling out of the Delfzijl plant by the end of 2029. That will provide the initial proof of concept for our low-carbon production model.

Gosse Boxhoorn: By 2036, we envision RESiLICON as the definitive market leader in the European polysilicon space. Given the exponential demand spikes driven by artificial intelligence (AI) in semiconductors, alongside the broader transition in solar and energy storage, Europe will require far more than a single polysilicon refinery. We hope our success will spark the deployment of four or five additional polysilicon facilities across France, Spain, and neighboring nations. True industrial resilience begins at the raw-material stage, and we intend to prove that European manufacturing can be clean, competitive, and entirely self-sustaining.

Establishing a completely self-sustaining domestic clean technology baseline requires both deep industrial endurance and major policy reform. RESiLICON stands as an admirable and necessary step away from total downstream reliance toward genuine upstream independence. By anchoring their clean, gas-phase refinement processes right at the landing point of offshore wind developments in Delfzijl, the team is proving that European manufacturing can match ecological responsibility with strict commercial scale. As the organization moves toward its final investment decision in early 2027, we remain highly optimistic about this pioneering effort to secure the very building blocks of our clean energy future.